A Buy In A Bazaar Place

Bazaarvoice (BV) hasn’t been on the public market scene for all that long, having completed its IPO just under 24 months ago. The stock is a very interesting play in the SaaS market, providing solutions that capture and analyze various word of mouth ratings, QA, and recommendations about brands and products.

Since IPO’ing, Bazaarvoice has had quite a ride in those short two years. It quickly broke $20/share, but soon found itself trading below $7 in early 2013. Investors can’t quite buy the company that cheap today, but they are getting it for a steal at under $10.

(click to enlarge)

There’s been a lot going on at the company over the past year, including the DOJ lawsuit that knocked shares to below $7 in January. Since then we’ve had a lot of positives that have been masked by the DOJ overhang. As a result, the stock is trading at an unjustified discount. We see fair value as $13.50, but $20 as easily achievable over the interim.

Switching up the business model

Late last year Bazaarvoice snatched up Longboard Media. This signaled a shift in the company’s business model. Longboard now brings a transactional aspect to the Bazaarvoice business model. Longboard is an ad network. The other key is that it broadens Bazaarvoice’s total asset market to include an even bigger portion of display advertising. The company believes the digital ad market opportunity is $100 billion market, compared to the $160 million it currently holds.

Source: WPP/GroupM Digital Advertising study March 2013

The acquisition looks to give BV a leg up on its competition in the fast-growing e-Commerce advertising market. The competition in social media marketing has only been increasing and we’ve seen big companies like Salesforce (CRM) and Oracle (ORCL) looking to get into the space. Salesforce purchased Buddy Media, which allows companies to publish their content seamlessly through Salesforce’s CRM software across all social media platforms. Oracle purchased Vitrue, which is now delivered via the Oracle Cloud and unifies social monitoring, marketing and engagement for its customers.

Where BV gets the leg up on its competition is through its ratings and review system. Before, BV provided its customers (20% of the Fortune 500) with information on their ratings so that they could improve their marketing and RD. With the Longboard acquisition, BV can combine its ratings with Longboard’s advertising network and allow companies to better target their customers, both potential and existing.

We look at it this way, the online company that can best harness customer data and direct that in targeted marketing, will win the war. This is the foundation that Google (GOOG) was built on and we like the steps that Bazaarvoice is taking to capture its share of a $100 billion market. The acquisition of Longboard allows Bazaarvoice to start monetizing its vast customer behavior database. That’s the key here and something that we think Mr. Market is seriously missing.

(click to enlarge)

Hitting on all cylinders

Just last month, we got more good news from the company, in our eyes, nonetheless. Some of the other great news is that the company closed Target as a customer, which is the third largest retailer in the U.S. Bazaarvoice has also been looking to break into over-the-pond markets, i.e. the U.K. And it’s seeing the first signs of positive traction by locking up Staples U.K. as a customer for Bazaarvoice Media. Other notable recent customer signups include Michelin, PPG Industries, Kellogg, and TOMS Shoes.

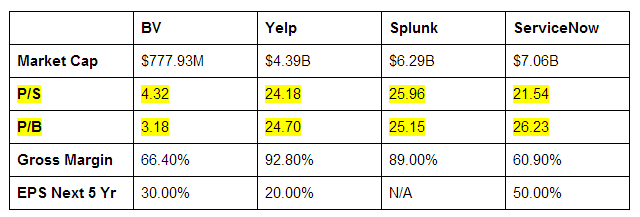

Here’s how BV stacks up with other SaaS providers.

(click to enlarge)

Not too bad right? As you can see, BV trades at ridiculously low multiples on a P/S and P/B basis compared to Yelp (YELP), Splunk (SPLK) and ServiceNow (NOW). This gets even better when we look at some of Bazaarvoice’s direct comps. Two of Bazaarvoice’s top pers are Pluck and Jive Software (JIVE). Demand Media (DMD) owns Pluck.

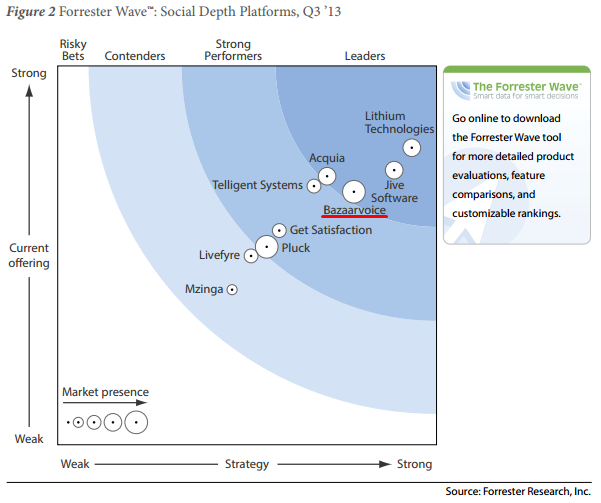

Jive trades at an EV/sales multiple of 5.6x, and Demand Media is at 6.4x. Meanwhile, Bazaarvoice trades at 4.6x EV/sales. Forrester Research has also come out and labeled Bazaarvoice as one of the market leaders per its July report, The Forrester Wave: Social Depth Platforms. Bazaarvoice got a 5-out-of-5 rating for reviews, analytics, ease-of-use, international support, etc. This should go a long way for creating awareness around the company, including getting chief marketing officers to take notice and consider the return on investment impact of Bazaarvoice services.

(click to enlarge)

Even if we look at Gartner’s Magic Quadrant, Bazaarvoice is still a top pick in the social CRM industry. It’s second only to salesforce.com when it comes to ability to execute. And is well above the likes of Demand Media (Pluck). Bazaarvoice also has a partnership with salesforce for identifying issues within reveiws and creating a service case for resolution.

Bazaarvoice really operates in a niche part of the market, where, although Pluck is considered a top comp, it operates in a different part of the market. Bazaarvoice is a provider for hosting ratings and reviews, while Pluck is a provider for hosting blogs, profiles, and photo galleries.

DOJ overhang creates catalyst

The DOJ’s lawsuit is related to Bazaarvoice’s acquisition of PowerReviews. The DOJ is making the case that the move decreases competition, monopolizes to some degree, the online review industry. Bazaarvoice remains optimistic on the outcome, but hasn’t offered any guidance on the potential costs. Here’s the underlying guidance from the company:

“On January 10, 2013, the U.S. Department of Justice filed a complaint against the Company with the U.S. District Court for the Northern District of California, San Francisco Division, alleging that the Company’s acquisition of PowerReviews violates Section 7 of

the Clayton Act, 15 U.S.C. Section 18 and seeking the Company’s divestiture of assets sufficient to create a competing business that can replace the competitive significance of PowerReviews in the marketplace. The Company disputes the allegations and intends to vigorously contest the matter. It is not possible to reliably predict the outcome of the case. Therefore, the Company cannot currently estimate the possible loss or range of loss that could result from the case.”

Ultimately, if Bazaarvoice loses, the company will have to spinoff its PowerReviews assets. It appears the market is applying a discount to Bazaarvoice given the litigation overhang. And so, this is a key catalyst for the stock. Once the lawsuit is finally resolved, the shares should trade higher, even if it has to divest PowerReviews. It appears the market is already pricing in a worst case.

Investment thesis

We see the DOJ lawsuit as being a case of – where would the stock be trading at if the DOJ never filed the suit? Bazaarvoice Chairman Tom Meredith pretty much summed up the company’s view of the lawsuit in his testimony at this month’s trial. He said (emphasis ours):

“I think in my deposition I used a phrase that might be cast as earthy, I think I called it B.S. That the notion that by acquiring PowerReviews, a company with $11 million in revenue in a nascent space would enable us, Bazaarvoice, to control pricing is ludicrous. I find it staggering that we’re even here having this conversation but I’m willing to go down this path.”

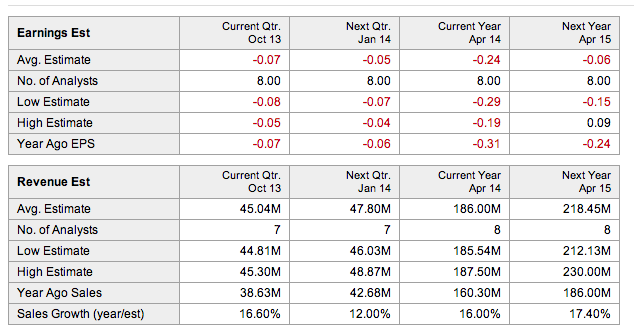

In looking at BV from a margin, price and earnings perspective, there are many things to like about the company. BV posted a gross margin of 70.5% in 1Q. While operating margins remain negative, that’s because the company is still unprofitable. However, losses have been narrowing and next year the company is forecasted to post an EPS loss of $0.06 compared to expectations of an EPS loss of $0.24 this year.(click to enlarge)

Source: Yahoo! Finance

While the company has been posting losses, the good news is that the company has been beating earnings expectations each time. Furthermore, over the next five years, EPS is expected to grow 30% year over year.

(click to enlarge)

Revenues are forecasted to grow to $218 million next fiscal year from an estimated $186 million this fiscal year. This further shows the company’s tremendous growth since its founding in 2007 when it posted $3 million in revenues.

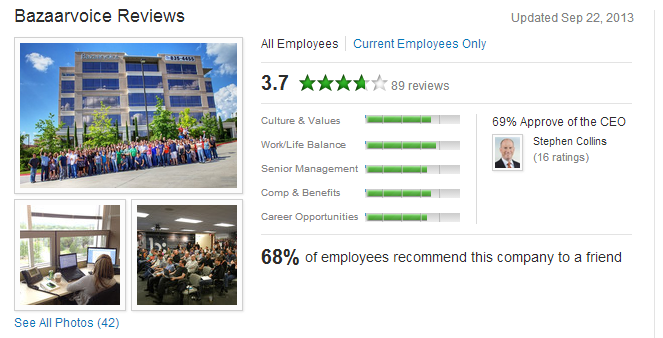

It doesn’t stop there. All around, Bazaarvoice appears to be a top notch company. Employees have a near 70% rating for CEO Stephen Collins and almost 70% would recommend the company to a friend. Compare to the 55% of employees that would recommend Demand Media.

(click to enlarge)

The other key to Bazaarvoice is that it’s very much a growth story. Its business model is highly scalable and EBITDA could easily grow exponentially. Putting the opportunity in perspective, assuming that Bazaarvoice can generate some $120 million in FCF over the long-term (over five years out) — based on roughly $300 million in sales — we see fair value as somewhere around $13.50. That assumes a roughly 15% discount rate and a 3% long-term growth rate.

Bottom line

Relief from the DOJ investigation, which is expected to come by month end, should provide a near term boost for the stock. The lawsuit has been a distraction for the company and has been a drain from both a management and cash flow perspective. In 1Q, cash used from operations was $9.2 million, of which $6 million was related to the DOJ lawsuit and shareholder litigation lawsuits.

The company is in the early stages of completing its software buildout. And so, it’s no surprise that earnings continue to run negative. We look for another couple years of negative earnings as the company completes front end migration. On the back-end, the company is already seeing marked improvement, generating 66% gross margins over the TTM.

Meanwhile, the company is hitting on all cylinders when it comes to attracting new customers, and should be trading closer to $13.50 in the near term. Longer term, once the dust settles and the company can go about ramping up its sales force, increasing product development and leveraging its client network, we see revenue growth further accelerating and leading shares back to its old highs north of $20.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Interesting article. database consulting can save money though

Thanks