")

")

Summary

- Shares of YELP have been under pressure amid mixed operating and financial trends.

- The company remains profitable, but is facing a decline in its restaurant and retail category advertising business.

- The stock’s deep valuation discount to larger tech peers may be justified given weak financial trends and more uncertain outlook.

We last covered Yelp Inc. (NYSE:YELP) in 2022 with a bullish outlook citing improving earnings at the time, in what, we believed, would be a banner year for the online crowdsourced business review and directory platform.

A lot has changed over the period. It turned out that 2023 was Yelp’s breakout year, which saw shares climb to a 5-year high before reversing those gains. The stock is currently down around 5% from our original call and also 31% lower from its 52-week high.

Our update today downgrades the stock with a more bearish view. As we see it, despite steady growth and consistent profitability, several core operating metrics stand out as concerning. We believe the company’s long-term outlook and growth potential have deteriorated, with risks tilted for further downside. Here are 4 reasons we recommend avoiding Yelp stock.

1) Poor Brand Momentum

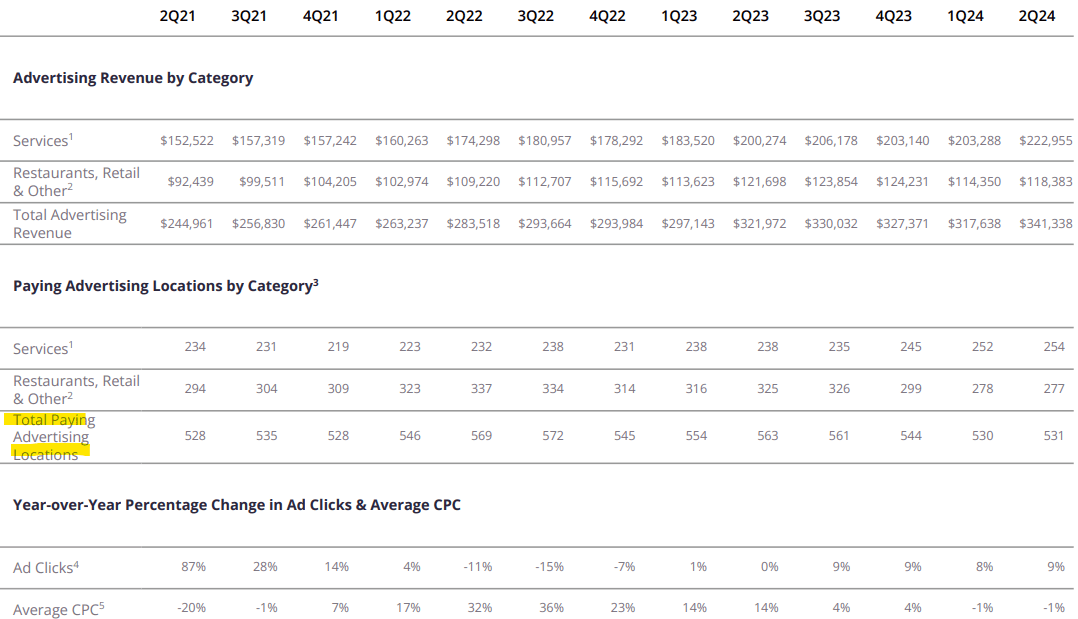

A major theme for Yelp has been a shift in its advertising mix, away from restaurants, retail & other (RR&O) towards the services category that covers small businesses like home repair, plumbers, electricians, and beauty salons.

The trend has had a favorable impact on total revenue which reached $341 million in the last reported second quarter, up 6% year-over-year, driven precisely by a 15% increase in services. On the other hand, the decline in revenues from the RR&O category is noticeable, down -3% year-over-year and sequentially over the past three quarters.

In our view, the problem is that Yelp is losing its total number of paying advertisers by location as a proxy for “customers”. The 531k total at the end of Q2 is down -6% y/y with the 7% increase in the number of service providers on the platform outweighed by the -15% y/y drop in RR&O locations. Moreover, the total number of paying advertised locations has been flat, going back to pre-pandemic levels.

The concern here is that Yelp is becoming less relevant in its traditional core market of restaurant reviews, which has important implications for site traffic and even the future potential in the service side of the business. If RR&O-type paying businesses are systematically leaving the platform, the risk is that the trend accelerates as remaining businesses begin to see lower user engagement and conversion.

There is also a question of how much more upside there is long-term with services, where despite Yelp managing to generate a higher average revenue per location, the number of providers is relatively constrained by city and region.

While the company doesn’t share user data, we can extrapolate its ad clicks metric where even with a 9% y/y increase this past quarter, with Yelp pointing to improvements in its algorithm, the total number of ad clicks is approximately flat from levels in early 2022. In the company’s Q2 shareholder letter, management anticipated the “year-over-year changes in ad clicks and average CPC since the second half of 2023 will moderate” due to more difficult prior-year comparisons.

2) Lower Quality Earnings

The other side of those soft operating metrics is the company’s effort to improve profitability, with some measure of success. Yelp’s $91 million in adjusted EBITDA for Q2 was 9% higher than last year with a 26% margin, up from 25% in Q2 2023.

That being said, the main factor contributing to that uptick was a decline in product development (PD) and general & administrative (G&A) costs as management moved to generate some financial efficiencies. These steps are commendable and show some initiative, but are not necessarily sustainable as a profitable growth strategy long term, particularly if the platform is struggling to retain paying advertisers.

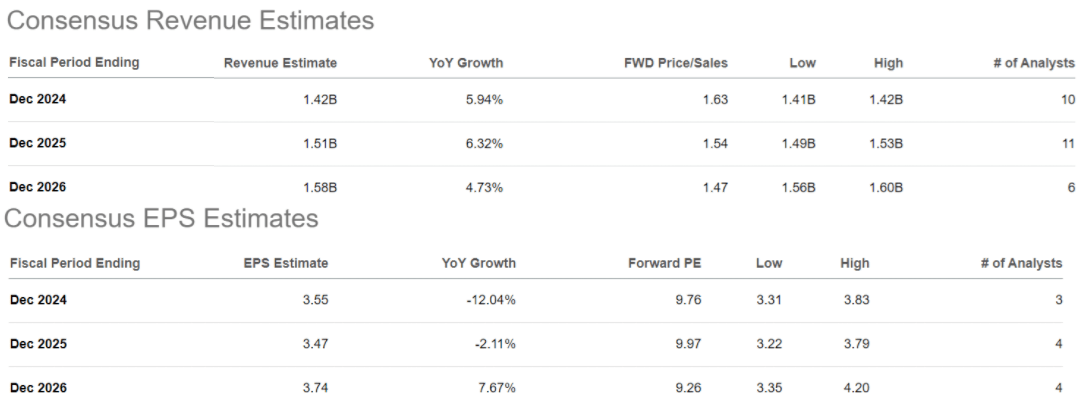

For the full year, Yelp expects net revenue of around $1.42 billion, marking a 6% increase from 2023. The adjusted EBITDA full-year estimate at a $330 million midpoint estimate is less impressive, just flat for 2023.

The big question and uncertainty for Yelp will be how its RR&O business evolves and whether it can keep the Services ecosystem robust against a highly competitive landscape that includes specialized players like Angi Inc. (ANGI) or OpenTable as a subsidiary of Booking Holdings Inc. (BKNG).

According to consensus, Yelp is forecast to generate mid-single-digit annual revenue growth through 2026 while EPS faces the headwind of ongoing CAPEX and development costs.

3) Yelp Could Be A Value-Trap

Ultimately, Yelp’s main competition is from larger tech players including Meta Platforms, Inc. (META), and Alphabet Inc. (GOOGL) which can leverage social media presence and search engines as an alternative for consumers to seek information and reviews, also representing an important advertising channel for all types of businesses.

Ultimately, it’s very hard for Yelp to compete with sites like Facebook.com, Instagram, and Google Search for businesses to reach potential customers. We can add that advancements in artificial intelligence, where people can ask a chatbot directly for a restaurant recommendation, have further diminished Yelp’s visibility which isn’t the authoritative source of reviews it may have been 10-15 years ago.

Some investors may look at Yelp trading at just 10 times its full-year consensus EPS, or an EV to forward EBITDA ratio of 6x as a relative bargain next to these same tech giants. In our view, this deep discount is more than justified given Yelp’s poor operating trends and the number of long-term uncertainties.

A Bearish Take On Yelp

We rate YELP as a sell with an expectation the ongoing share price selloff will continue. The risk for the stock is that further weakness in the RR&O advertising category, coupled with weaker-than-expected trends in the services market side of the operation, would lead to revisions to lower the company’s earnings outlook.

At the same time, we’ll be the first to come back here and admit we got the narrative wrong if Yelp manages to drive higher its total number of advertising locations and generate sharply stronger operating margins as key monitoring points. The stock could rally on evidence that revenues are accelerating as a tailwind for earnings.